AI Is Redistributing Economic Power – Even as Capital Concentrates

“While consensus says AI centralizes talent, the opposite happens: AI makes micro-entrepreneurship viable at scale.”

– Sasha McKenzie, Wellington Access Ventures (Axios Pro Rata)¹

Capital Concentration Is Real – and Measurable

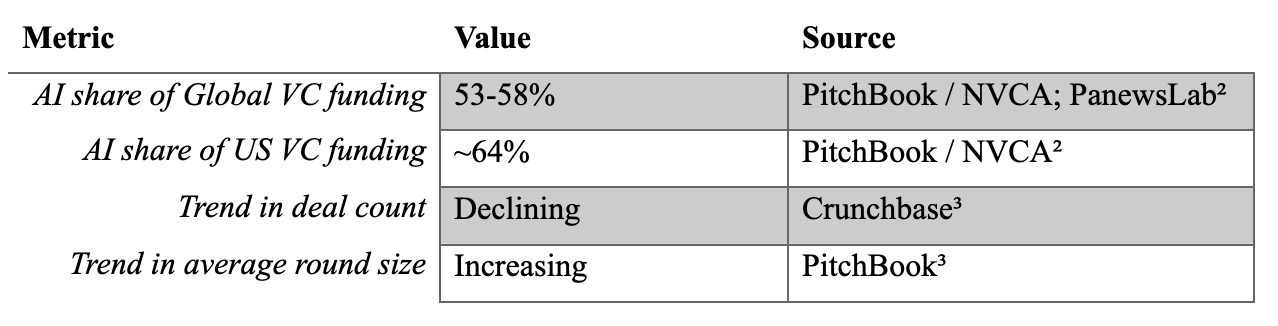

In 2025, Artificial Intelligence received the largest total dollar amount of investment from venture capital in history. Data from PitchBook, the National Venture Capital Association (NVCA), and Crunchbase show that AI companies received between 53% and 58% of global venture capital and approximately 64% of U.S. venture capital funding. Despite the increasing investment in venture capital, the total number of deals being made has gone down. Several smaller companies are receiving much larger rounds of funding, particularly at the foundational model and infrastructure layers. Although capital is increasingly concentrated in the hands of the few, this does not directly indicate where economic agency is located.

Table 1. Selected AI Market Indicators (2025)

These figures clearly support the claim that capital is concentrating. They do not, on their own, establish that economic agency is centralizing.

Falling Costs Enable Wider Participation

Due to the continued development of AI models because of increased training and new technology, there has been a decrease in the cost of developing AI models. For example, OpenAI’s Chief Executive, Sam Altman, has stated how the costs of inference have reduced 10 times in the last few years.4 Major models pricing histories support this; costs are reduced in relation to tokens, and throughput has been higher. By decreasing the upfront development costs, expanding and experimenting with current AI models becomes less risky.

However, developing new AI models is still a very expensive venture. For example, training next-generation large language models can cost over $1B or more per training run.5 Epoch AI and other scaling analyses substantiate this. Due to these incredibly high costs, only the largest hyperscalers can bear the risk of developing new AI.

Empirical Evidence of Micro-Entrepreneurship

Research analyzing the spread of AI-native products shows that areas with AI-related skills have drastically more small firms, as opposed to large ones, which would have traditionally dominated those spaces in the past.6 AI has been able to stimulate entrepreneurship not only in tech centers and incubators but also across expansive geographic areas.

Information gathered from various independent founders corroborates this trend, Indie Hackers and Stripe Atlas have found numerous cases of small teams with six and seven figure ARR, even in the absence of institutional funding.7 While these may not be representative of the median, or indicative of a coming trend, they prove that this style is viable.

Enterprise AI Adoption Is Becoming More Selective

Even though there will be an increase in spending for enterprise AI and in the development of AI-native products, this does not mean there will be an increase in the number of AI products gaining this funding.8 A select few players will come to dominate the market share; however, these will not be generic generalists, but specialists with a dedicated purpose. In fact, CIO surveys suggest a departure from these generic generalists to AI with more specific outcome-driven applications.

Due to the presence of a flywheel effect, which enables specialists to reach greater utility and efficiency for their tasks faster than the generalists, the smaller, narrower models can outperform the larger ones at specific tasks. This demonstrates how agency can be distributed even in places where the capital is aggregated. Meaning that smaller AI with specific use cases have unique viability in the marketplaces allowing the startups that develop these AI to flourish.

Labor Market Dispersion and Adjacent AI Services

Recently, there has been a departure from the overcompensation of AI specialists in the labor markets, a trend that was prominent in 2024 and 2025 with the construction of Meta Superintelligence Labs. Increasingly, talent has begun to depart from traditional labs and research stations in favor of startups and independent ventures (LinkedIn Economic Growth and Levels.fyi).9

The date labeling and model evaluation sectors have also seen an explosion in growth. Turing, an AI service company, tripled its revenue and made $300 million.10 This highlights the fact that value in AI can also be found outside of the leading model businesses.

AI Flywheels and Compound Advantage

In certain situations, the decentralization for winner-take-most scenarios is reinforced by a strong mechanism – the AI flywheel: The more users engage with a model, the more behavioral data is generated, which can be used to improve the quality of a model, enhance personalization, and minimize the error rate.

This feedback loop is evident in various scenarios:

A. Recommendation Systems

Systems that improve recommendations based on user interactions, such as TikTok, YouTube, and Spotify, become more entertaining as they collect more data. Improvements in quality, driven by user interactions, compound to increase both retention and engagement.

B. Autonomous Agents and Productivity Tools

AI models have been continuing to improve as they get feedback via input from users and validation from human/AI overseers. This continuous refinement allows for the AI to get better over time, and it enables it to become more efficient.

As more users interact with the AI, its capabilities will continue to be enhanced. This will make it more efficient, and will allow it greater utility. A major benefit of this is the fact that it is completely fueled by data as opposed to dollars. However, this can also be a setback as it is dependent upon user engagement which often fluctuates based on demand.

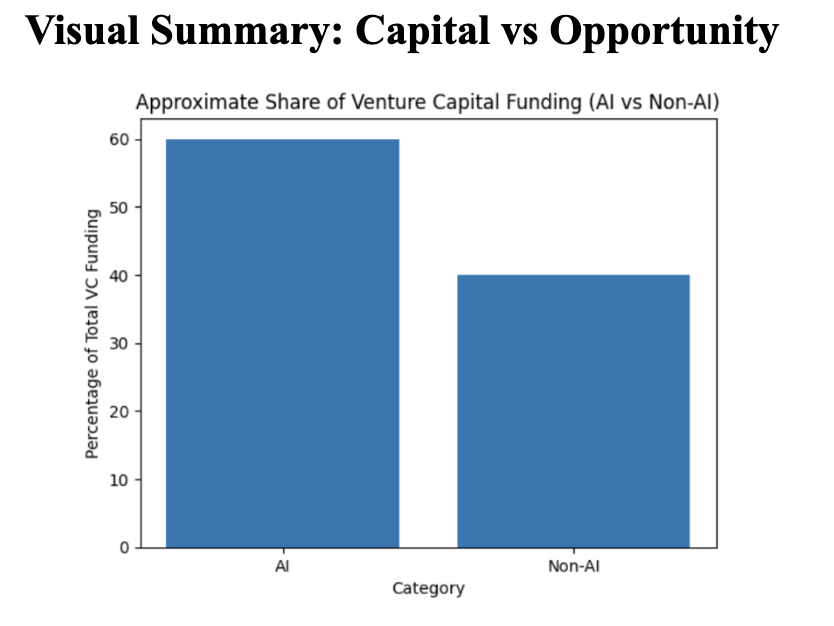

Visual Summary: Capital vs Opportunity

Figure 1. Approximate Share of Venture Capital Funding (AI vs. Non-AI, 2025) (Based on aggregated PitchBook/NVCA data.)

While AI dominates the allocation of capital, the presence of opportunity is still shaped by cost, data access, and the flywheel. These factors combine to influence where economic agency materializes.

Conclusion: A More Nuanced Reality

The impact of AI is not a clear pathway of centralization or decentralization. Rather, it is a combination of various interrelated factors. These include: centralization of capital and data-rich platform domains (search, recommendations); decentralization in application layers, where low cost and operational accessibility empower small teams to develop sustainable businesses; flywheel effects that may amplify both central advantages (for platforms) and niche advantages (for specialized applications). As Sasha McKenzie states, AI can and does facilitate micro-entrepreneurship.

As this new trend continues to surface, understanding the underlying conditions and implications associated with this concentration and distribution will be vital to discerning scalable opportunities.

* Written by Henry Cyr, Gotham Chi at UChicago Member